Article Category and Author

Admin

Share

New Listings Today

What Cape Coral’s Unfolding Drama Means for North Carolina’s Real Estate Future – Echoes from the Eye of the Storm:

The national real estate narrative often feels like a distant hum, but occasionally, a specific locale becomes a focal point, a crucible where market forces are distilled into raw, undeniable reality. For many, Cape Coral, Florida, holds that distinction. In the mid-2000s, its rapid, speculative boom, fueled by easy credit and unchecked development, made it a widely recognized “ground zero” for the 2008 housing collapse. Today, as signs point to a new, albeit different, period of significant correction, its story once again casts a long shadow, prompting a vital question: how will the evolving turmoil in this Sunshine State hotspot uniquely affect the robust markets of Charlotte, Lake Norman, and Asheville, North Carolina?

Cape Coral: The Crucible of Correction, Then and Now

In the lead-up to 2008, Cape Coral’s picturesque canals became the arteries of a speculative frenzy. Investors and eager buyers, many with little to no down payment or income verification, flocked to the area, driving prices to unsustainable heights. When the subprime mortgage crisis hit, the “house of cards” collapsed. Foreclosures surged into the tens of thousands, properties lay abandoned, and the city became a stark emblem of the Great Recession’s housing devastation.

Fast forward to 2025, and Cape Coral is once again under the microscope. After another pandemic-era boom that saw values jump over 70% in five years, the market is turning. Recent analyses in July 2025 describe Cape Coral as one of the worst housing markets in the U.S. Home prices have plummeted, falling by as much as 11% in the past two years, with declines recorded in 12 out of 13 recent months. Inventory has surged dramatically—up 525% since 2022, reaching months of supply well into buyer’s market territory (7.3 to 12.3 months, and even 7.8 months for Lee County overall). Over 50% of listings are seeing price reductions, and a concerning number of homeowners are “underwater” on their mortgages. While the drivers are different this time (high interest rates, oversupply from new construction, and affordability issues, rather than predatory lending), the outcome for many sellers is distressingly familiar: a sustained correction.

North Carolina’s Resilient Landscape: A Different Trajectory

In contrast to Cape Coral’s dramatic swings, North Carolina’s major markets demonstrate a more measured, fundamentally driven growth:

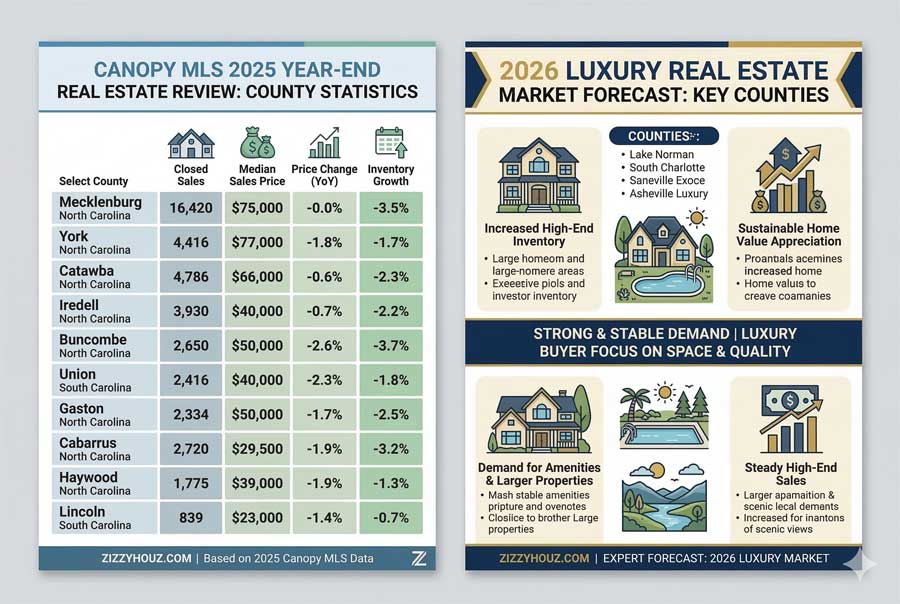

- Charlotte: While seeing a recent slowdown, Charlotte’s market is primarily shifting towards balance, not collapse. After years of strong appreciation, some areas saw a modest year-over-year home value decline (e.g., -0.4% in Mecklenburg County in 2025), indicating a cooling from peak highs. Inventory is rising, and days on market are lengthening, giving buyers more choice and negotiation power. However, it’s still fundamentally strong, buoyed by consistent population influx and a diversified economy.

- Lake Norman (e.g., Huntersville, Mooresville): This attractive region continues to see strong demand, though some pockets are adjusting. While parts of Lake Norman in Iredell County saw a median sale price decrease (-21.0% YoY in May 2025), this can be influenced by luxury sales mix. Generally, homes are selling for around 2% below list price after longer days on market (66 days vs. 45 days a year ago), reflecting a transition from an intense seller’s market to a more balanced one, but generally with underlying appreciation and robust buyer interest.

- Asheville: The unique mountain city is also experiencing a shift towards a more balanced market. While overall Buncombe County saw a slight median price decline in Q1 2025, the City of Asheville itself saw a modest increase (+3.9% in April 2025). Inventory is increasing, and days on market are extending (40 days average in June 2025 vs. 33 days a year ago). Asheville remains highly desirable, and its adjustments are largely a normalization from peak frenetic activity.

These NC markets, built on strong job markets, diverse industries, and sustainable population growth, present a stark contrast to Cape Coral’s more speculative past and present.

The Ripple Effect: Unconventional Ways Cape Coral Touches NC

The direct impact of Cape Coral’s specific market woes on Charlotte, Lake Norman, or Asheville is minimal, given their distinct economic foundations. However, the indirect and often overlooked ways this Florida turmoil can affect North Carolina are fascinating:

- The “Behavioral Contagion” of Caution: Beyond direct economic ties, market sentiment is highly contagious. When a well-known “ground zero” like Cape Coral experiences significant price cuts and a glut of inventory, it sends a psychological ripple through national news cycles. This doesn’t mean NC homes will crash, but it can instill a heightened sense of caution in both buyers and sellers. Buyers might become more emboldened to negotiate, making “over-asking” bids rarer. Sellers, in turn, may become more proactive in pricing competitively from day one, internalizing the lesson that even in strong markets, ignoring fundamentals can lead to stagnation. This fosters a healthier, more rational market environment.

- The “Migration of Disillusionment”: Cape Coral’s severe correction could, over time, contribute to a “migration of disillusionment.” Individuals or even smaller investment groups who experienced the boom-bust cycle there might seek out markets that offer more predictable, sustainable growth. North Carolina, with its perceived stability, diverse economy, and attractive lifestyle, could subtly benefit from this redirection of attention and capital from those wary of future Florida volatility. It’s not a flood, but a gradual, deliberate trickle of informed relocation.

- The “Developer’s Due Diligence Dividend”: The painful lessons from Cape Coral’s oversupply and speculative building during its previous boom (and potentially its current one) serve as a stark reminder for developers and city planners nationwide. For North Carolina, this translates into a “due diligence dividend.” Local authorities and developers might approach new projects with a keener eye on demand-supply equilibrium, sustainable infrastructure, and less on pure speculation, thus avoiding the pitfalls of overbuilding that contributed to Cape Coral’s woes. This fosters a more resilient, well-planned housing inventory for NC’s future.

- The “Equity Exodus” for Downsizing/Relocation: Some homeowners in markets like Cape Coral who are not “underwater” but have seen their equity diminish might decide to sell now, before deeper corrections, and seek out new beginnings in different, more stable regions. North Carolina could become a prime destination for these “equity exiles” – individuals who decide to cash out what they can and reset their lives in a market offering greater peace of mind. Their motivation isn’t to chase speculative gains, but to find stability, potentially adding a unique segment of cautious, value-oriented buyers to the NC market.

While Cape Coral’s current struggles are significant, they offer North Carolina’s real estate markets less of a direct threat and more of a valuable, albeit indirect, learning experience. The echoes from the Eye of the Storm in Florida serve as a powerful reminder of market cycles, promoting a healthier sense of realism, and potentially re-directing a more discerning type of buyer and investor towards the comparatively grounded opportunities that Charlotte, Lake Norman, and Asheville continue to offer.

Full Advanced Search

Editor's Pick

What Our Customers Say

“I went under contract on my home, one hour after he listed the property.”

"Brent Dillon is the reason that the process of selling of my home and buying a new home in Florida went flawlessly. Brent was there every step of the way, guiding me and making me [...]